- Humber to Warwickshire Oil Storage (Kingsbury)

- Humber to Jarrow

- Milford Haven to Westerleigh, Theale and Bedworth (Murco)

- Grangemouth to Dalston, Cumbria

DB Shenker, which acquired EWS, is the main freight train operator in this sector, with Freightliner also represented.

– by coaster

Coasters move between 3000-20,000 mt of product. While both Shell and BP still operate marine tanker fleets, the principal operator is James Fisher & Sons. The latter, has a fleet of 18 tankers ranging in size from 3500-13,000 DWT and carries over 8 million mt to UK-wide locations each year.

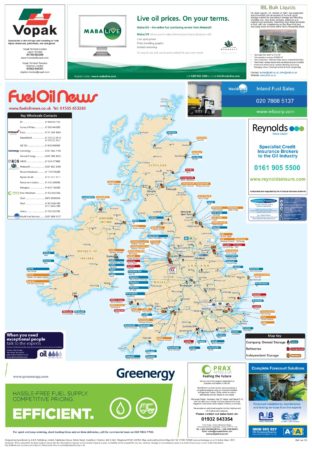

Rationalisation at storage and distribution terminals

Coryton looks set to join the 50 distribution terminals which currently serve theUKinland market, after Shell, Greenergy and Vopak announced a joint venture to convert the refinery into an import and storage facility.

The changing trends affecting the refinery network over the past 30 years, have also been in evidence at storage terminals. As various players have rationalised their geographic market presence, numbers have shrunk with fewer, larger locations covering the market.

There has been a clear trend towards retreating to refineries as key distribution points. In part, this was driven by the outcome of the Oil Warehouse Review in 1985 and enactment of legislation that moved the excise duty liability from terminal to refinery gate.

The reduction in mainline distribution points is exemplified in the following regions:

Manchester/Mersey conurbation – 13 down to 4

Yorkshire- 6 to 0

East Anglia- 6 to one for high flash products only

Through all this change, the system’s resilience has been a continuing source of reassurance. Ample testimony of its resilience was provided by its adaptation to the loss of the key Buncefield facility, almost seven years ago.

Following the cessation of crude oil processing operations at Coryton, the infrastructure’s robustness may well be tested once again. Readers’ views as to resilience are invited – jane@fueloilnews.co.uk.