Three of the six refineries in the current network (Fawley, Grangemouth and Stanlow) can trace their origins back to the 1920s with the other three facilities (Pembroke, Lindsey and Humber) being commissioned in the post-WW2 era, through the 1950s and 60s – the major growth phase of the downstream sector.

As a result, by the start of the 1970s, the network comprised 18 plants but, since the last of the existing network was commissioned by Conoco (now Phillips 66) on Humberside, in 1969, this network has seen 12 closures, with a total nameplate capacity of 60 million tonnes with half of the closures occurring during the 1980s.

By way of indulgence in a bit of nostalgia, the table to the right summarises those which are no longer with us.

As a result of the above closures, the two formerly largest ‘players’ in the sector, BP and Shell, have, since 2011, ceased to have any UK refining presence.

We will now take a brief look at the existing network and highlight the roles which they play in supplying refined petroleum products to the inland market.

Present: Now there are six – the current refinery network

Last year, UK refineries supplied about 85% of the country’s inland market requirements.

One of the key features of the network, which has a total throughput capacity of circa 56 million tonnes per year, is that it is misconfigured vis-à-vis inland market requirements; net exports of petrol represent around 40% of refinery production, while net imports of diesel represent around 50% of inland requirements and, in the case of Jet A-1, about two thirds of requirements.

Four of the six facilities have undergone rationalisation/ optimisation programmes over the past ten years, in the form of reductions in nameplate capacities. Taking the constituents of the network individually, in descending order by capacity:

Fawley:

Capacity was reduced in 2012, by about 20%, through closure of one of the distillation units to just over 13 million tonnes per year and it is estimated to supply around 15% of the country’s refined products requirements.

The lion’s share (circa 85%) of its output is moved to four inland distribution terminals through a 450-mile owned pipeline network to:

– Staines.

– Purfleet.

– Avonmouth.

– Bromsgrove.

Road tanker deliveries from the refinery into the local market are made from a loading facility at Hythe. The balance is transported by coaster.

It therefore comprises a substantial, and critical, source of supply to the major markets of the south, south east, Bristol/Avonmouth and the Midlands as well as to Heathrow and Gatwick airports.

Humber:

Nameplate capacity is just under 11 million tonnes per year through two distillation units, with around 70% of the refinery’s production being placed in the UK inland market:

- by coaster to Scotland (e.g. Aberdeen & Inverness), Tyneside and East Anglia.

- by the Exolum pipeline (formerly GPSS) to Bramhall terminal in south Manchester.

- by rail to Warwick Oil Storage Ltd. at Kingsbury.

- by RTW from nearby Immingham terminal, servicing local markets in Humberside, Yorkshire, the North East and Lincolnshire.

The refinery is Europe’s sole supply source (and one of the world’s largest) of premium grade petroleum coke, a key material not only in steel and aluminium manufacture but also for lithium-ion batteries.

Co-processing used cooking oil to produce renewable diesel was started in 2017, at 50,000mt/year, subsequently expanded to 150,000 mt/year, with further expansion to 250,000mt/year in 2024. Earlier this year an agreement was reached with BA to supply SAF from the refinery in to the Exolum (CLH) pipeline.

Pembroke:

Nameplate crude oil distillation capacity is about 10.5 million tonnes per year, with the refinery boasting one of the largest FCC units in Europe (circa 4 million tonnes per year). Refined products are distributed to three main channels:

- The UK inland market

- Ireland, where it is the single largest supply source

- East coast USA (petrol)

Deliveries to the domestic market are made by:

- Pipeline, where products are shipped by the Mainline Pipeline, owned 100% by Valero since 2012, along a 300-mile system to the company’s terminals at Kingsbury and Trafford Park, Manchester.

- Coaster, where products are shipped to Valero’s three sea-fed terminals in Avonmouth, Cardiff and Plymouth.

The refinery also supplies Jet A-1 at a number of airports including Heathrow, Gatwick and Stansted.

Stanlow:

Capacity was reduced in 2014 from just over 14 million tonnes per year to 9 million tonnes by closure of one of the crude distillation units as an optimisation measure. A subsequent, major turnaround exercise, in 2018, increased throughput capacity to over 10.2 million tonnes per year.

It is estimated that the refinery supplies approximately 17% of the country’s road transport fuels, by three main modes:

- Pipeline, where products are supplied in to the UKOP system for shipment to Kingsbury terminal and also further south, via a twin line built by Shell in the early 1980s, to enable movements via Buncefield, principally to Heathrow and Gatwick airports. Jet A-1 is supplied directly to Manchester airport through the Manchester Jet Pipeline.

- Road, by road tankers from Stanlow Terminals, servicing the north west.

- Coaster, where products are lifted by tankers via the Manchester Ship Canal.

The refinery is also a supplier to the petrochemical industry, providing feedstocks such as toluene, propylene and ethylbenzene.

Grangemouth:

Rationalisation measures, initiated in late 2020, comprised the closure of a distillation unit, reducing overall capacity from around 10.2 million tonnes per year to 7.3 million tonnes, and the shut-down of a 1 million tonnes per year FCC unit.

The refinery provides around 70% of Scotland’s refined oil requirements and products are moved out by five principal routes:

- Road, supplying the lion’s share of the requirements of filling stations across Scotland as well as the Jet A-1 needs of the three main airports, Edinburgh, Glasgow and Aberdeen.

- Rail, to the Petroineos distribution terminal at Dalston, near Carlisle.

- Pump-over, into the adjacent Exolum public storage facility.

- Pipeline, to the Finnart Ocean terminal on the west coast for lifting by tanker.

- Coaster, for lifting by tanker.

Closely integrated with the refinery, which is a key feedstock source, is the adjacent petrochemical complex, which produces polyethylene, polypropylene and other industrial solvents and chemicals.

Lindsey:

Capacity was halved in 2015, to 5.4 million tonnes per year, with the closure of one of the two crude oil distillation units and, in 2020, Total sold the refinery, along with associated distribution assets, to the Prax Group.

The main channels of product distribution to the UK market are as follows:

- Road, from the refinery road loading facility to RTW’s servicing markets in the north, north

- east, Humberside/Lincolnshire and East Anglia.

- Rail, to co-owned (with Phillips 66) Warwickshire Oil Storage terminal at Kingsbury and to the Prax terminal at Jarrow.

- Pipeline, for the carriage of Jet A-1 along the 145-mile Finaline to Buncefield and onward movement to Heathrow airport.

- Coaster, from APT, Immingham (jointly owned with Phillips66) to east coast UK locations.

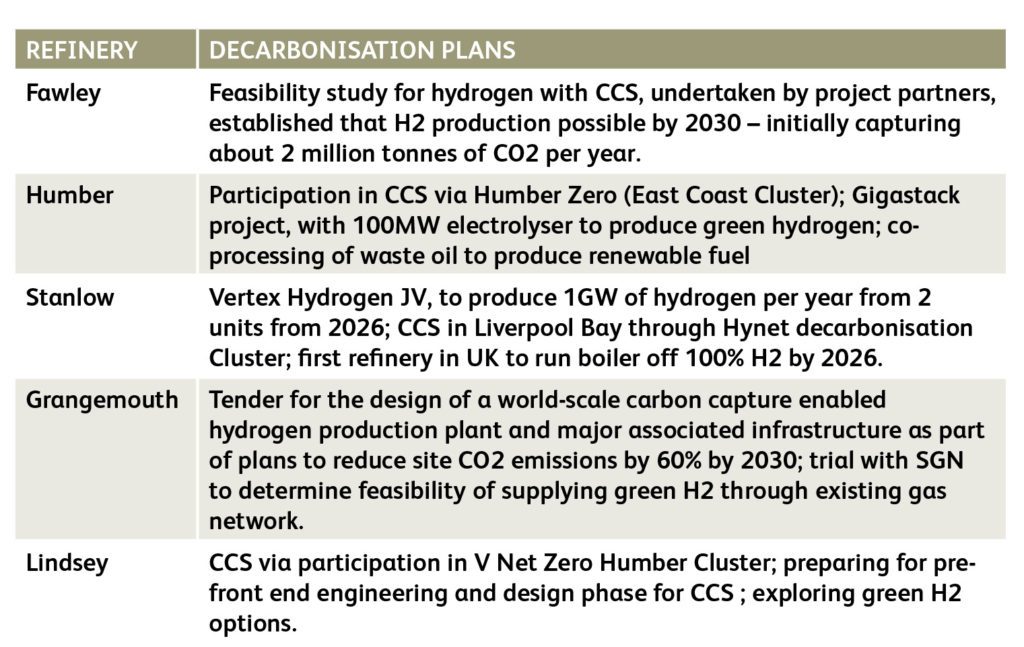

Decarbonisation projects

Having highlighted the capacities of the constituent refineries and the distribution channels through which products are supplied to the market, we will now get a flavour of some of the decarbonisation initiatives being pursued. These are summarised in the table below:

From the table, it is clear that the refining sector is actively embracing the ‘decarbonisation agenda’, in particular CCS and the potential of hydrogen. No doubt there will be further initiatives which will be pursued as the energy transition evolves?

The future

For the past 50+ years the UK refinery network has provided an uninterrupted, secure and reliable supply of petroleum products which have played a critical role in ‘keeping the economy’s wheels turning’. This role will continue for the foreseeable future, albeit diminishing in terms of quantities supplied as the energy transition gathers pace.

The events of 2022 have underscored the need for energy security, with an indigenous refinery network being a key component thereof. In the course of time, three changes to the network are possible:

- Conversion of an existing petroleum refinery/ refineries into bio-refineries- to produce a range of sustainable low carbon biofuels

- More extensive adoption of co-processing to produce biofuels

- Closure, either permanent or conversion to a product import terminal

Time will tell the extent to which these developments take root and, indeed, more broadly, what kind and size or shape of network will evolve as refined oil product demand declines.

The UK refinery network has shown its adaptability to changing requirements over the past 50 plus years; this resilience will provide a strong foundation to meet the coming challenges of both the ongoing need for security of product supply and the energy transition.

ROD PROWSE, worked for 30 years across the full spectrum of the downstream oil sector, in both the UK and USA, which has included leadership positions in both retail and wholesale fuels businesses. Rod draws on his extensive knowledge of this global industry to bring us ‘Industry Insights’.