News

Portland Market Report – oil prices

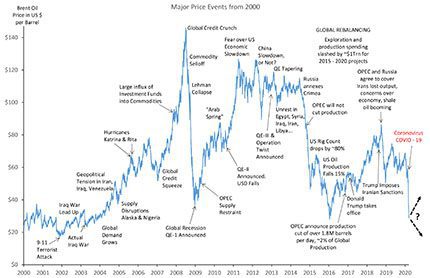

At the beginning of this year, we put together our annual prediction for oil prices and those who read it will remember that it was largely bearish in tone. Our thinking was that just as oil production was increasing, the global economy was showing sure signs of a slow-down. We also pointed out that OPEC’s surprisingly steadfast cohesion, was now under threat, with certain member states (along with Russia) increasingly fed-up with the continued production cut regime.

What we didn’t fully appreciate when we wrote the report was that these factors would be background noise, once the impact of Coronavirus (then it is early stages and pretty-well confined to China) started to take a grip. To put it mildly, the Coronavirus has hit oil (and stock) markets like a whirlwind and all at a rather inconvenient time for the global oil industry. We discussed the impact on demand last month, with consumption down by about 2-3m barrels per day (bpd) in February alone, but worse was soon to come when Saudi Arabia and Russia became embroiled in a spectacular supply side spat.

Relationships within OPEC have been increasingly discordant for several years now, but they reached breaking point at March’s OPEC meeting in Vienna. Saudi Arabia basically accused fellow OPEC members (and Russia) of playing a duplicitous game when it came to production cuts. The Saudis believe that only they have fully cut production (and thus pushed up prices), whilst their OPEC colleagues have simply paid lip-service to the idea and in fact have aimed to increase production, whilst “filling their boots” at the higher prices. Russia’s counter view was that not only had they been diligent in enforcing their own production cuts, but more significantly, further cuts would have little effect anyway in the face of mass demand drop-off caused by the Coronavirus.

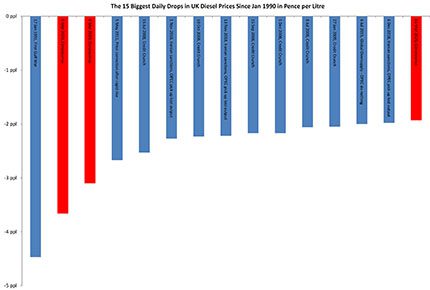

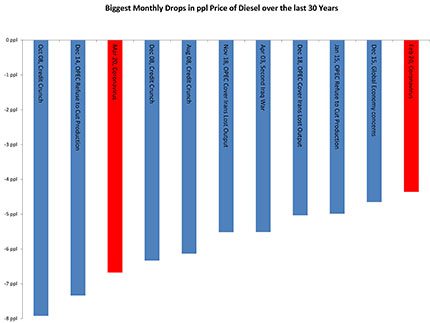

Cue one of the most bad-tempered OPEC meetings in recent history as tempers rose and harmony vanished in a morass of name calling, finger pointing and general throwing of toys out of prams. As the meeting broke asunder, Saudi Arabia didn’t just confirm that the production cut regime was over, they went on to announce that the kingdom would be increasing their production by 45% (ie, from 9m bpd to 13m bpd). The result on oil markets was as electrifying as it was catastrophic. On the day of the announcement, oil prices fell by $8 per barrel and the following Monday, by a similar amount. These falls in price (see graphs) were the biggest single day drops since at least 1990 and (if we had the records) probably way before that.

So where next for oil prices? In the short-term, we can safely discount any recovery in consumer demand pushing prices back upwards quickly. Clearly, as long as Coronavirus has its grip on Government policy across the world, then lock-downs remain the order of the day, which in turn means consumption is severely constrained. At a macro level however, there could be support for oil prices from the large, strategic buyers, who are now looking at attractively low oil prices. The two biggest strategic buyers of oil in the world are the oil reserve companies of the USA and China respectively, both of whom are currently holding less stock than they are legislatively obliged to hold. Therefore, they need to boost stocks and what better time to do that than now, with prices much lower than at any point in the last 10 years?

However, even a major buying spree based on the above scenario will be less important to the market’s direction than the behaviour of the world’s major oil producing nations over the next few weeks. Saudi Arabia’s decision to increase production remains the key factor. Even if the markets have already “priced in” this excess volume (this was the reason for the huge price drops), when the extra oil actually starts to flow and the market literally becomes flooded with oil (tankage full to the brim, tankers full of oil and anchored outside ports with nowhere to discharge) it seems impossible to predict anything other than a continued bearish market.

One might wonder then, whether the Saudis are now heavily regretting opening this particular Pandora’s box? After all, the drop in oil prices has now gone way beyond simply punishing Russia and putting US producers out of business. It is now drastically hurting Saudi Arabia itself and remember, it was only in December that Saudi Aramco became the biggest IPO in history. It’s fair to say that recent private investors in the company will not be enjoying these low, low prices. So one possible outcome which will not be reported, might be for the Saudis to quietly walk away from their threat to increase production and simply keep things as they were. That won’t be enough to get prices rising again, but it would be the only thing that could stop prices falling much further.

Portland Fuel

www.portland-fuel.co.uk