For many fuel distributors, diversification is no longer a future ambition – it is already becoming part of day-to-day business strategy.

Across the UK and Ireland, distributors are steadily expanding beyond traditional fuel delivery into a wider range of complementary services, from AdBlue and lubricants to tank monitoring, HVO, fuel cards and renewable technologies.

In some cases, these services are relatively simple add-ons designed to improve customer retention and increase revenue per account. In others, they represent the early stages of broader business transformation as distributors respond to changing customer expectations, increasing competition and the long-term evolution of the energy market.

For SME distributors in particular, the challenge is not simply deciding whether to diversify, but which services offer the strongest commercial return without creating unsustainable complexity, capital strain or compliance risk.

This month’s Delivering Insight explores the complementary services already gaining traction across the sector, the opportunities and risks associated with expansion, and how fuel distributors can assess which additions genuinely strengthen long-term resilience.

Section 1: Diversification is becoming standard

Fuel distributors today are increasingly expected to provide more than fuel alone.

Customers now value convenience, integrated service packages and suppliers who can solve multiple operational challenges through a single relationship. For distributors, that creates an opportunity to deepen customer loyalty while reducing dependence on core fuel margins alone.

The trend is already visible across the sector.

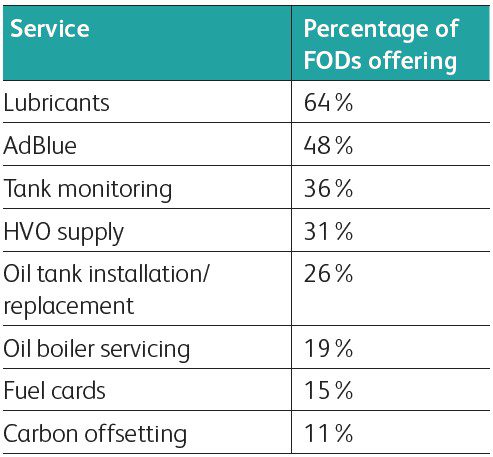

Fuel Oil News research published in the 2026 Yearbook showed that many distributors now offer a growing portfolio of complementary services alongside fuel supply.

The most commonly offered additional services are:

The research also highlights a clear relationship between company size and diversification breadth. Larger distributors are significantly more likely to offer higher-complexity or capital-intensive services, while smaller operators typically focus on lower-cost add-ons that integrate naturally into existing operations.

That distinction matters because not all complementary services carry the same operational burden, staffing requirements or payback profile.

Section 2: Why complementary services matter

The commercial rationale behind diversification is straightforward.

Additional services can:

- Increase customer lifetime value

- Improve customer retention

- Create recurring revenue streams

- Differentiate the business from competitors

- Reduce exposure to fuel demand fluctuations

- Strengthen long-term resilience during the energy transition

In many cases, the greatest value is not immediate profit margin, but the strengthening of customer relationships.

For example:

- Tank monitoring systems linked to auto-top-up services encourage repeat purchasing and reduce the likelihood of customers switching supplier

- Emergency delivery services can reinforce trust and loyalty during periods of market stress or severe weather

- Welfare-focused schemes such as priority delivery or payment support can improve retention among vulnerable domestic customers

- Tank installation and servicing often create follow-on maintenance and fuel supply opportunities over many years

The wider energy transition is also influencing diversification decisions.

Some distributors are expanding into renewable fuels such as HVO, while others are beginning to explore adjacent energy services including solar, heat pumps or EV charging. Although these remain relatively uncommon today, they may become increasingly important as customer energy requirements evolve.

Section 3: Which services offer the best opportunity?

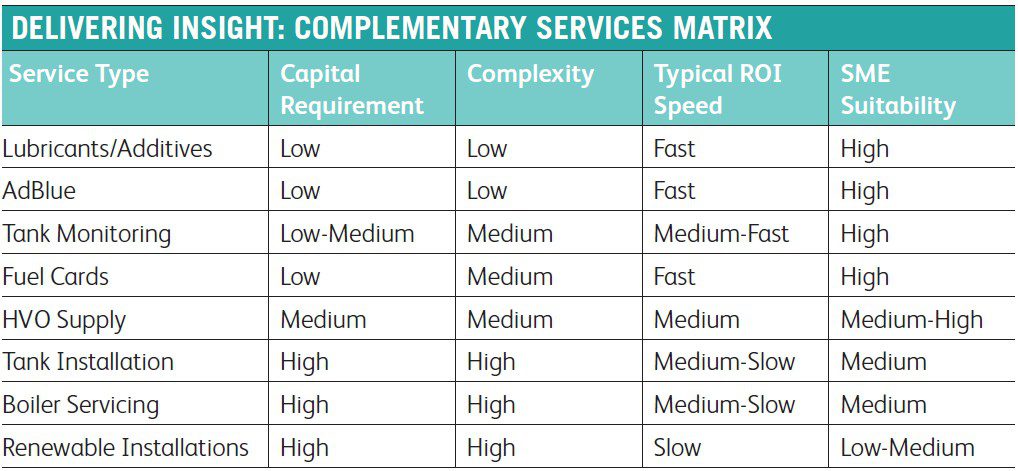

Not all complementary services are equal in terms of setup cost, operational complexity or return on investment.

For many SMEs, the strongest opportunities are often the simplest.

Low-capital, high-accessibility services

Services such as AdBlue, lubricants and fuel additives are attractive because they can often be integrated into existing delivery infrastructure with relatively low investment.

Advantages include:

- Predictable repeat demand

- Limited additional staffing requirements

- Faster payback periods

- Cross-selling opportunities with existing customers

- Minimal operational disruption

AdBlue in particular benefits from recurring demand linked directly to diesel fleet usage, while lubricants and additives can increase average order value with comparatively little additional operational complexity.

Tank monitoring systems also sit within this category.

Although telemetry platforms require investment in hardware, software integration and customer support, they can significantly improve delivery efficiency, reduce emergency callouts and strengthen customer retention.

For SMEs looking for a first diversification step, these lower-cost service categories often provide the most manageable entry point.

Medium-complexity expansion areas

HVO supply represents a growing middle-ground opportunity.

Demand for renewable fuels continues to increase across commercial fleets, construction, backup power and industrial applications. UK HVO supply volumes reportedly increased from 502 million litres in 2023 to 784 million litres in 2024, highlighting the rapid growth of the market.

For distributors, HVO can provide:

- Access to customers pursuing carbon reduction goals

- New commercial opportunities

- A future-focused positioning

- Retention of diesel customers seeking lower-carbon options

However, HVO also introduces supply chain, storage, pricing and technical considerations that require careful management.

Fuel cards can also offer attractive returns relative to their setup costs, particularly where distributors partner with established third-party providers rather than building infrastructure independently.

Higher-capital diversification

More infrastructure-intensive services carry greater potential reward but significantly higher complexity.

These include:

- Oil tank installation and servicing

- Boiler installation and servicing

- Renewable technology installation

- Generator supply and servicing

- Retail forecourts

These services often require:

- Specialist staff and training

- Additional compliance obligations

- Engineering capability

- Insurance considerations

- Larger upfront capital investment

- Expanded administration and management systems

For larger distributors, these areas may support long-term strategic positioning and broader energy-service evolution. For SMEs, however, they may be better approached through partnerships, acquisitions or phased rollout strategies rather than rapid expansion.

Section 4: Demand varies by customer sector

Complementary service demand differs significantly between domestic, agricultural and commercial customers.

Domestic customers

Domestic heating customers increasingly value convenience, reliability and support services.

Key opportunities include:

- Tank monitoring and auto-top-up

- Emergency deliveries

- Boiler servicing partnerships

- Tank replacement

- Customer welfare schemes

In periods of severe weather or supply disruption, these additional services can become important differentiators.

Agricultural customers

Agricultural customers often require broader operational support.

Demand areas include:

- Lubricants and additives

- Generator support

- Fuel quality management

- Long-term storage support

- Mixed equipment servicing

Remote operations and seasonal pressures can make reliability-focused services particularly valuable in this sector.

Commercial customers

Commercial and fleet customers are increasingly driven by efficiency, compliance and decarbonisation pressures.

Key growth areas include:

- AdBlue supply

- Fuel cards

- Usage monitoring and telemetry

- HVO integration support

- Fuel management systems

For these customers, data visibility and operational efficiency are often as important as fuel price itself.

Section 5: The risks of diversification

While complementary services can strengthen resilience, they also introduce new risks.

The most common challenges include:

Operational complexity

As service portfolios expand, businesses often require additional administration, scheduling, staffing and technical oversight.

Compliance exposure

New services may introduce additional regulatory obligations covering environmental compliance, engineering standards, electrical work, financial services or health and safety.

Working capital pressure

Inventory expansion, equipment investment and increased customer credit requirements can place significant strain on cash flow – particularly for SMEs.

Skills shortages

Some services require specialist expertise that may be difficult or expensive to recruit.

Dilution of focus

Diversification that lacks clear strategic alignment can create operational distraction without delivering meaningful commercial return.

For smaller distributors especially, there is a risk of attempting to diversify too broadly without sufficient operational capacity.

Section 6: Strategic expansion vs reactive expansion

One of the most important distinctions is whether diversification is strategic or reactive.

The strongest complementary services are typically those that:

- Align naturally with the existing customer base

- Build on existing operational capability

- Create recurring revenue

- Improve retention

- Strengthen long-term positioning

- Can scale sustainably

The weakest expansions are often those driven primarily by trend-following without sufficient demand analysis or operational planning.

That is why many distributors are increasingly adopting phased approaches, trialling services first through pilot schemes, partnerships or limited customer groups before committing to larger rollouts.

In practice, successful diversification often looks evolutionary rather than transformational.

Summary of findings

- Fuel distributors are steadily evolving from traditional fuel suppliers into broader service providers.

- Complementary services can improve customer retention, recurring revenue and resilience.

- Lower-cost services such as AdBlue, lubricants and telemetry often provide the most accessible diversification opportunities for SMEs.

- Larger distributors are more likely to pursue infrastructure-intensive services due to greater scale and capital availability.

- Diversification introduces operational, financial and compliance risks that require careful management.

- Strategic, phased expansion is typically more sustainable than rapid or reactive diversification.

Recommended actions for FODs

1. Analyse customer demand carefully

Assess which services align most closely with the needs of your domestic, agricultural and commercial customer base.

2. Start with low-risk opportunities

Prioritise lower-capital, higher-margin services that integrate naturally into existing operations.

3. Pilot before scaling

Trial new services with selected customers and monitor ROI, retention impact and operational strain before wider rollout.

4. Use partnerships strategically

Third-party partnerships can reduce capital exposure and specialist staffing requirements for more complex services.

5. Focus on customer retention, not just revenue

The long-term value of complementary services often lies in strengthening customer relationships and reducing churn.

Conclusion

Complementary services are becoming an increasingly important part of the fuel distributor business model.

For some businesses, diversification is about improving margins and customer retention. For others, it forms part of a broader strategy to prepare for long-term energy market evolution.

However, successful diversification is rarely about offering the largest number of services. Instead, the strongest approaches are usually those that build carefully around existing customer relationships, operational strengths and realistic growth capacity.

For SME distributors in particular, selectively adding one or two well-aligned services may deliver greater long-term value than attempting wholesale transformation too quickly.

In a changing market, resilience may increasingly come not from moving away from fuel distribution – but from building a broader, more valuable service proposition around it.