Feedstocks

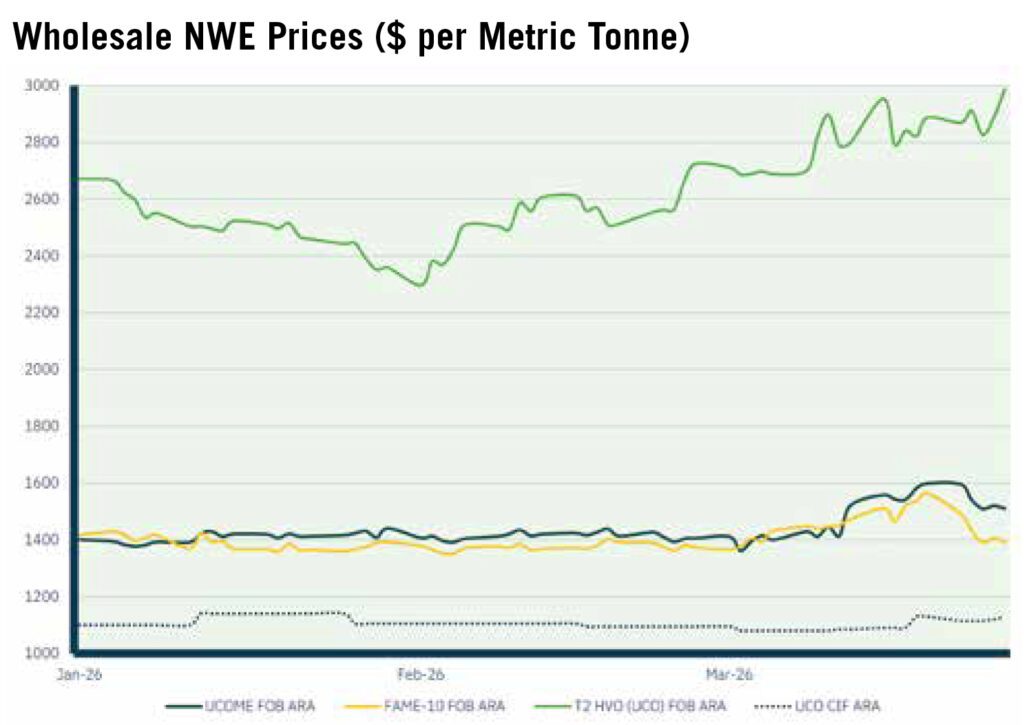

UCO prices recorded limited movement across Q1, increasing marginally from $1,100/mt to $1,135/mt (71.9-76.0ppl), remaining close to the three-year high of $1,160/mt (76.3ppl) reached in September 2025.

In January, Indonesia opted to increase export levies on POME and UCO, to protect supply and generate revenue for its domestic biofuel mandate and emerging SAF production, after POME exports reached 14 month highs due to strong demand from EU renewable fuel producers.

The increase follows reports that Indonesia may divert crude palm oil (CPO) volumes typically destined for export into domestic biofuel production, as part of an effort to exert influence over global CPO prices. Conflict in the Middle East and a domestic tallow shortage caused a price spike in US feedstocks, including UCO, leading to increased interest in US demand for Asian UCO, drawing volume away from European markets.

Biodiesel

Following a relatively flat market through much of January and February, a surge in Low Sulphur Gasoil Futures, the underlying price benchmark for European biofuels, driven by the outbreak of war in the Middle East, saw biodiesel prices rise in March. However, premiums above LSGO fell to their lowest levels in two years, causing certificate markets to decline across Europe due to the narrowing of the differential between mineral grades and biodiesel, with demand capped by EU limits on the bio content of road fuels.

Q1 2026 also marked a structural change in feedstock preference, due to the implementation of revised German and Dutch biofuels policies from 1st January (retroactively applied as the legislation continues to work its way through parliament). The new mandates have seen the value of waste-based biodiesels (e.g. UCOME) fall relative to those produced sustainably from crop (e.g. FAME-10) due to the scrapping of double-counting in these markets.

As a result, the UCOME price differential to FAME-10 fell into negative on several occasions throughout Q1, demonstrating the shift in demand for European biofuels blenders.

FAME-10 and UCOME

UCOME started the year trading at a discount to FAME-10, reaching a Q1 low of -$35.75/mt (-2.3ppl) on 3rd January, a trend that continued throughout the first half of the month as the premium on waste-based biodiesels dissipated due to the scrapping of double-counting, lowering the compliance value of UCOME relative to other grades.

However, an increase in UCO prices, compared to a relatively liquid rapeseed market, saw UCOME prices rise back above FAME-10 during the second half of January and throughout February, with the differential averaging $42/mt (2.7ppl) across this period. Conflict in the Middle East following US airstrikes on Iran commencing 28th February marked the start of a period of volatility, with FAME-10 prices quickly jumping, briefly seeing the UCOME differential fall into negative again.

However, it widened once more towards the end of the quarter as biofuels markets anticipated the announcement of higher US biofuels mandates, expected to drive up feedstock costs, in particular UCO. As a result, the UCOME premium above FAME-10 rose to a Q1 high of $148/mt (9.9ppl) at the end of March.

Market Outlook

Looking ahead to Q2, revisions to the US Environmental Protection Agency’s (EPA) Renewable Fuels Standard (RFS), under its “Set 2” regulations, are likely to impact HVO supply out of the US, the primary source for the UK in Q1 as it traded at a discount to the European market.

Therefore, despite the Trade Remedies Authority’s (TRA) decision in mid- March to recommend against countervailing duties on US HVO exports to the UK, the existing price arbitrage between US and European product is expected to narrow into Q2. A late amendment to the EPA’s renewable fuels policy also saw the current imported feedstock penalty scrapped, meaning biofuels produced from both domestic and imported feedstocks will be treated equally under the new regulations.

As the US does not produce enough feedstock domestically to meet the additional demand expected as a result of the revised RFS, the US will be reliant on imports to meet the new targets, which will likely impact the availability of feedstock supply to Europe, increasing production costs for HVO and first generation biodiesels such as UCOME.

HVO

Q1 was a period of uncertainty for HVO supply to the UK, with suppliers awaiting the outcome of the TRA’s anti-subsidy investigation into US HVO.

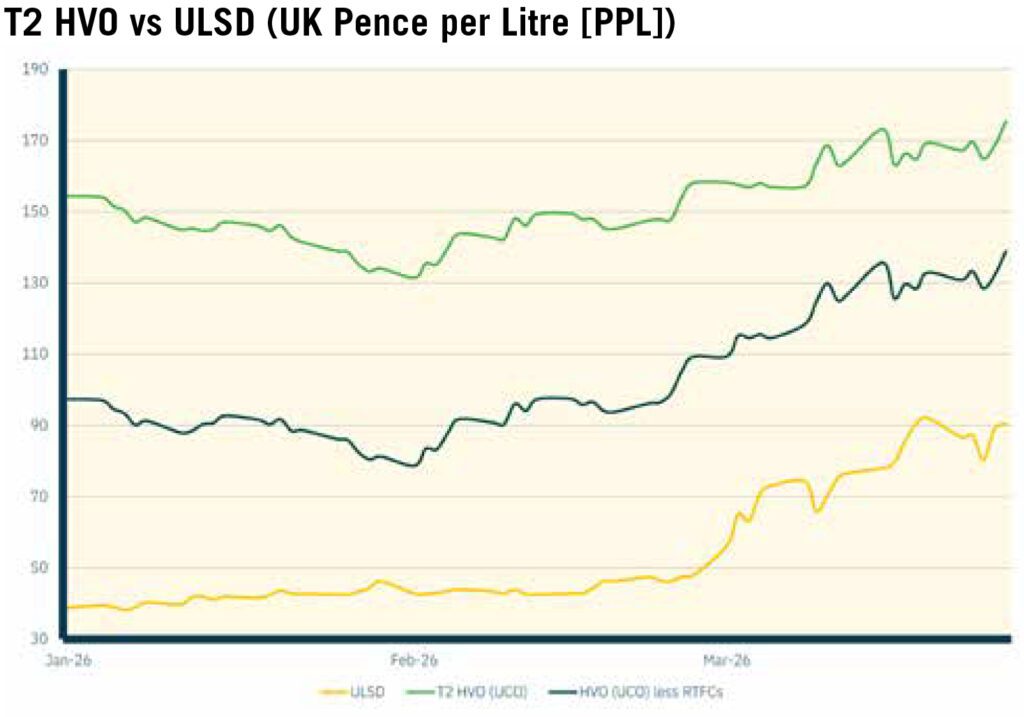

Following its initial Statement of Essential Facts issued at the end of November 2025, the TRA initially recommended duties of between 20-23ppl to be applied. As a result, throughout Q1, T1 (non-EU) cargoes were being offered with varying levels of TRA duties protection (50% or 100%), which saw the price gap to T2 (EU) product narrow, albeit still at a discount.

Following the TRA’s U-turn, the gap reopened, however the EPA’s announcement of its “Set 2” RFS regulations saw the differential narrow once more towards the end of the quarter. Wholesale T2 prices for UCO-derived HVO rose by $330/mt (23.5ppl) across Q1, reaching a three-and-a-half year high of $3,007/mt (177.9ppl) by the end of March, driven by a combination of high underlying LSGO prices due to the Iran War, and an expected increase in demand from the revised RFS. The price impact of the conflict in Iran was tempered to some extent in the UK by high inventories held by UK suppliers, causing the UK price to be depressed, with an incentive for suppliers to reduce stock levels to avoid severe backwardation costs.

However, a significant drop in the value of RTFCs saw T2 prices net of RTFCs rise to 145.0ppl, the highest level since October 2022. The RTFC benefit on waste-derived HVO fell from 57.0ppl to 32.8ppl across Q1, an increase of 24.2ppl on the final cost of HVO for UK end users.

Certificates

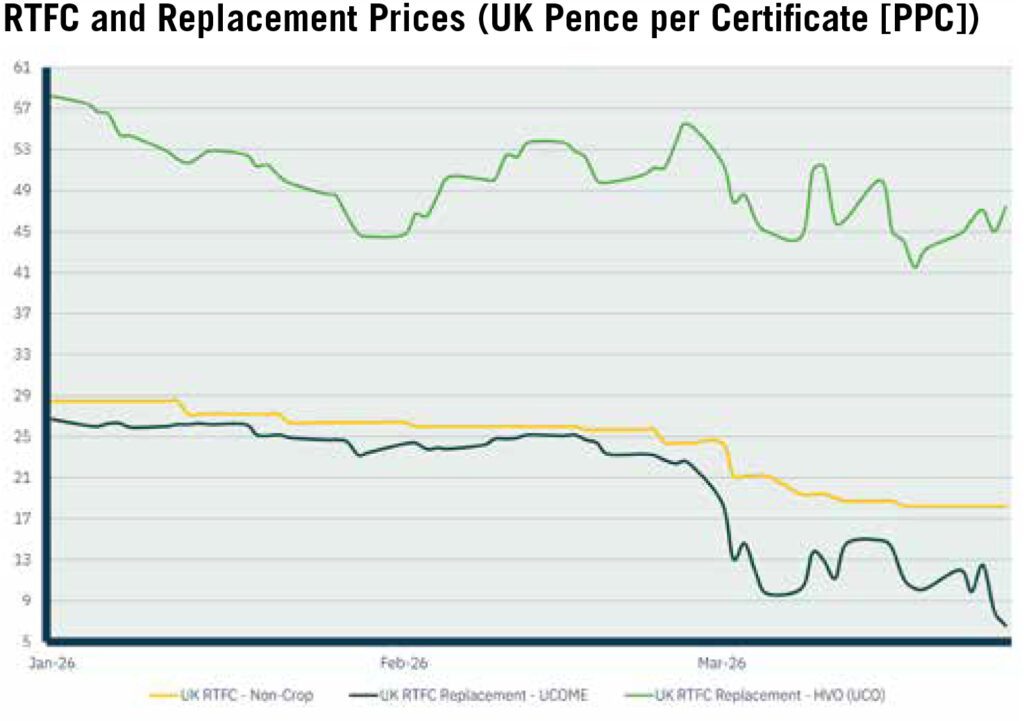

After starting 2026 at a 33-month high of 28.50 pence per certificate, non-crop RTFC prices fell throughout Q1, ending March at a two-year low of 16.40ppc.

The decline in certificate prices was largely due to rising diesel costs across the quarter, which saw the differential between biodiesel and mineral diesel narrow, reducing the cost of blending. This was particularly prevalent throughout March, following the outbreak of war in the Middle East at the end of February.

Non-crop RTFC prices fell by 8ppc in March, with the differential between mineral diesel and UCOME, the primary biodiesel blendstock used to generate certificates declining by 85%. However, with the diesel futures market in greater backwardation, the differential widens again down the forward curve, lending support to RTFC prices and creating dislocation between non-crop RTFCs and UCOME RTFC replacement prices.”

News and Policy

The TRA concluded its anti-subsidy investigation into US HVO on 12th March, deciding that no countervailing duties should be imposed, ending a period of uncertainty for UK HVO supply. The TRA initially recommended duties of 20-23ppl on US HVO imports, before ultimately reversing its decision on the basis that US HVO production is no longer being subsidised following the expiry of the Blenders Tax Credit at the end of 2024.

The decision may be open to appeal due to the 45Z credit, which effectively replaces the BTC, although the challenge over ‘like products’ remains. The US Environmental Protection Agency has announced record-high biofuel mandates under its revised “Set 2” Renewable Fuel Standards, causing a surge in RIN (US biofuel credits) pricing and a subsequent upturn in domestic production of renewable diesel and biodiesel.

Higher targets in the US are likely to impact the availability and price of exports to the UK, with local demand expected to soak up supply from US producers. Additionally, the new regulations have scrapped a penalty on imported feedstocks, meaning the US is likely to turn to the global market for supply.

Indonesia raised export levies and duties on refined UCO and POME, key feedstocks used in biodiesel production, for three consecutive months across Q1 2026, in order to support its domestic blending mandates. Plans to move to a B50 target were shelved in January, however policy-makers are reconsidering due to the recent spike in fossil fuel prices.

This is in addition to a blanket ban on exports of raw UCO and POME introduced in 2025, following reports that the country was exporting more than its total production capacity, leading to concerns over feedstock fraud.

info@eslfuels.com 0151 601 5201 www.eslfuels.com

Image credit: ESL Fuels, Dreamstime