Feedstocks

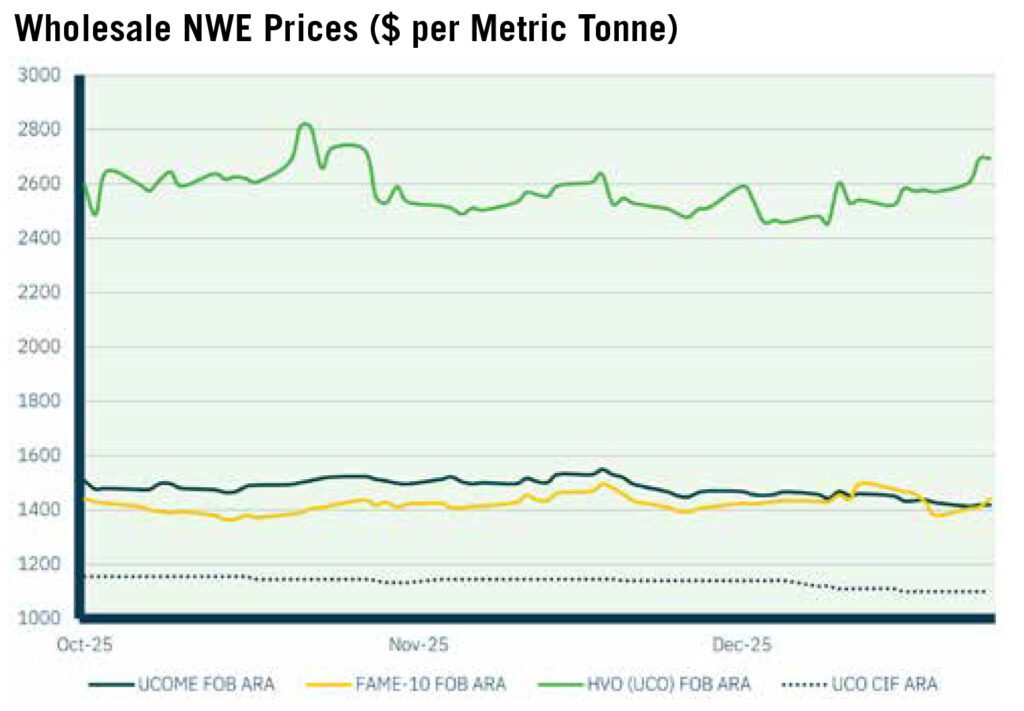

UCO prices were relatively stable between October and November, moving from $1,155 to $1,140/mt (75.5-75.9ppl), remaining near the three-year high of $1,160/mt (76.3ppl) reached in September amid high demand for HVO and SAF.

Reports that Indonesia could raise its export levy on UCO also supported prices, as the country seeks to fund its SAF ambitions. In the US, uncertainty remains around the impact of changes to the 45Z Clean Fuel Production Tax Credit on supply flows, although market participants expect US biofuel producers to increasingly turn to domestic feedstocks due to restrictive biofuel and trade policies.

However, Chinese exports reached an eleven-month high due to stronger sales to both Europe and the US, alleviating supply concerns. Towards year-end, trading slowed on policy uncertainty, dampening demand and causing UCO prices to fall to $1,100/mt (72.2ppl).

Biodiesel

UK biodiesel imports fell to a six-month low in October, with reduced supply from Europe and Asia, including a sharp drop in shipments from China following the UK’s anti-dumping investigation. Domestic consumption also eased as local suppliers increasingly relied on buying RTFCs to meet blend obligations.

In November, biodiesel prices remained under pressure from falling Low Sulphur Gasoil futures, although strong rapeseed demand (the key feedstock for RME and accounting for 90% of FAME-10 pricing) helped limit losses, as well as being indirectly supported by rising domestic biofuel demand in Brazil and the US.

Towards the end of the quarter, February 2026 rapeseed futures in Paris softened slightly amid higher supply from Canada and Australia, while global production forecasts were raised to a record 95 million tonnes (exceeding the previous season by almost 10 million tonnes). Finally, rising exports of UCO from China to the US and Europe also contributed to lower biodiesel prices, as this key feedstock became more widely available.

FAME-10 & UCOME

A rally in the first half of October saw the UCOME premium to FAME-10 widen from a low of $46/mt (3.0 ppl) to reach a Q4 peak of $119/mt (7.8 ppl), with UCOME prices supported by a strong UCO feedstock market due to cross-sector compliance demand, whilst FAME-10 prices fell by around 5% in the same period, reaching a quarter low of $1,364/mt (90.8 ppl) on 14th October.

However, the differential then gradually fell across the remainder of Q4, as colder weather saw demand for winter-grade biodiesel increase and the premium for waste-based biodiesels faltered as markets prepared for the scrapping of double-counting to be confirmed in Germany.

UCOME prices eventually fell below FAME-10 for the first time since February 2023 in mid-December, after the proposed revisions to German national biofuels policy were finally confirmed, reducing the comparative GHG reduction value between the two grades. After reaching a low of -$40/mt (-2.6 ppl) on 29th December, the UCOME premium to FAME-10 recovered slightly to close the year at -$11.50/mt (-0.8 ppl), with UCOME at $1,410/mt (92.5 ppl) and FAME-10 at $1,422/mt (93.3 ppl).

Market Outlook

After a year of change for the European biofuels landscape, with amendments to several key national policies following the enforcement of RED III in May 2025, 2026 will be a period of adjustment as supply chains adapt to both a general increase in biofuels and other renewable fuels demand (a result of higher targets), and a shift in requirements to now higher rewarded GHG reduction fuels following the confirmed scrapping of double-counting in Germany and the Netherlands.

This will reduce the premium for waste-based biodiesel such as UCOME against other methyl ester biodiesels, in particular those produced sustainably from crop. Due to blending limitations on methyl ester biodiesel, this will also drive demand for drop-in products such as HVO, the effects of which have already significantly impacted prices throughout the second half of 2025, a trend that is unlikely to ease in the coming year.

The biofuels feedstock pool is also likely to become wider and more diverse due to an increase in advanced sub-targets, as policy-makers seek to encourage the development of next-generation biofuels due to feedstock limits in existing production pathways.

HVO

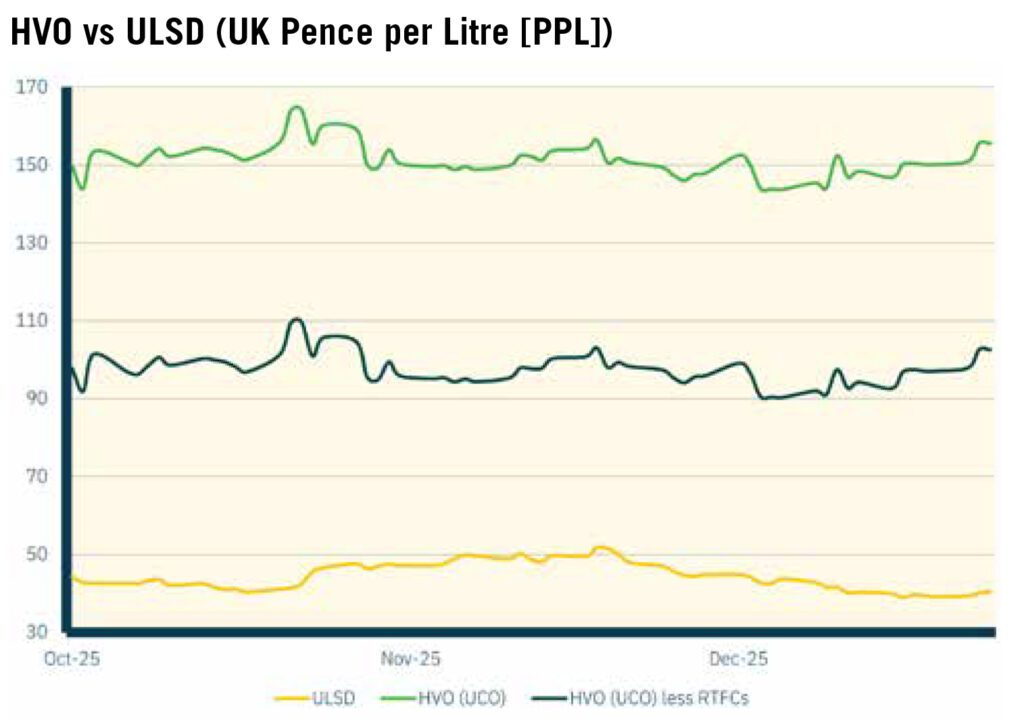

The UK market continued to import T1 product from the US, which trades at a discount to the Northwest European (T2) published wholesale price of HVO produced from UCO. The latter continued its upward trajectory in Q4, driven by increased compliance demand as the market prepares for higher European biofuels obligations in 2026.

Prices reached a three-year high of $2,810/mt (163.9 ppl) on 22nd October on supply tightness into the final quarter of 2025. Prices then saw a slight decline through November and into December, falling to a Q4 low of $2,455/mt (144.0 ppl) as demand softened and production levels stabilised following planned refinery maintenance at the start of the quarter.

HVO prices then recovered to $2,750/mt (159.4 ppl) by the end of December, after the German cabinet met to approve proposed changes to its national biofuels policy in line with RED III, ending a period of uncertainty for the European biofuels market. T2 prices net of RTFCs peaked at 109.62 ppl in October – the spike in wholesale prices was exacerbated by an uptick in the value of RTFCs, which rose to 27.25 ppc in the second half of the month, increasing the benefit to UK HVO buyers by 2.5 ppl due to double-counting.

This saw the differential to mineral diesel widen to 68.0 ppl. Whilst the differential narrowed into November, reaching a Q4 low of 44.7 ppl, a steep decline in mineral diesel prices towards the end of the quarter saw it widen once more, with UK HVO closing December 66.8 ppl above mineral diesel.

Certificates

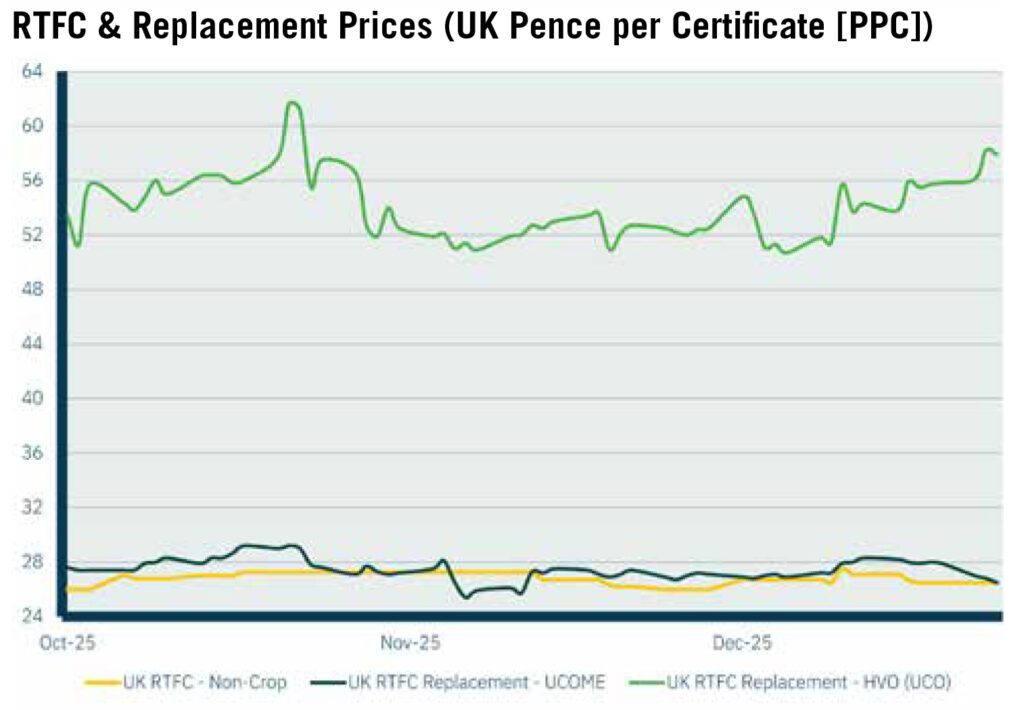

Despite an overall decline in biodiesel prices in Q4, particularly UCOME, the key blend stock used to comply with the Renewable Transport Fuel Obligation (RTFO) and therefore the effective price setter for RTFCs, non-crop certificate prices held firm throughout the quarter, trading in a narrow range of 26.0 to 27.5 ppc.

This is due to the much steeper decline in diesel prices across the period, a result of oversupply concerns in the broader oil markets. As such, the gap between fossil and bio products widened, increasing the cost of blending and in turn the cost of meeting the RTFO and subsequent certificate value. Theoretical RTFC replacement prices for HVO produced from UCO spiked in October, reaching a Q4 high of 61.60 ppc, in line with rising outright HVO costs.

News & Policy

Targets for meeting the UK’s Renewable Transport Fuel Obligation (RTFO) will increase from 1st January, raising the volume share of renewable fuels required to be supplied to the UK market. The main obligation will rise to 14.054% in 2026, up from 13.563% in 2025, whilst the Development Fuels Obligation (DFO, the advanced subobligation within the RTFO) rises from 1.619% to 1.863%.

The RTFO is currently under review, with proposed changes expected to be announced in 2026, with an implementation target of 2027, subject to industry review.

The UK Trade Remedies Authority (TRA) published its Statement of Essential Facts in late November, on HVO imports from the US, finding that subsidised imports are causing material injury to UK biodiesel producers. The TRA has proposed a fixed countervailing duty between £257.80 and £303.56 per tonne, with a final recommendation due in March.

An industry response is likely to object to the proposal, raising concerns such as the absence of a domestic industry producing HVO and the impact of further price increases on imports to the UK market.

Provisional data released by the Department of Transport (DfT) in November highlighted that verified renewable fuels supplied to the UK reached 2.4 billion litres in the first ten months of 2025. According to S&P Global, biofuels now account for an estimated 6.8% of the UK’s total transport fuel supply, indicating continued growth in supply and demand.

Within the renewable fuel mix, bioethanol is the largest contributor at around 1.1 billion litres, followed by biodiesel at 519 million litres and HVO at an estimated 408 million litres.

info@eslfuels.com 0151 601 5201 www.eslfuels.com

Image credit: ESL Fuels, Dreamstime