Although larger distribution groups may have in-house HR teams, fleet managers, compliance officers and analysts, many SME FODs operate without those resources. Delivering Insight is your virtual support team – a growing knowledge base that builds into a valuable reference library for your business, helping you make informed decisions that safeguard your business today and strengthen it for the future.

The fuel industry has undergone major shifts in recent years and continues to evolve in response to fluctuating demand, shifting consumer habits and policy change to achieve a Net Zero transition. The domestic heating markets in the UK and Ireland are no exception, and consumer buying patterns are changing with it.

Fuel Oil Distributors (FODs) have long relied on predictable buying behaviour to manage stock levels, ensure operational efficiency, and maintain profitability. To ensure long-term resilience, FODs need a clear view of how the sector has changed, and the factors most likely to shape its future. This article explores how purchasing in the domestic heating market has transformed over time, helping you to adapt in order to stay ahead of the curve.

Kerosene demand

Kerosene, or “heating oil”, is used for domestic heating in an estimated 1.5 million UK homes, representing 5% of all homes. Additionally, an estimated 680,000 homes currently use heating oil in the Republic of Ireland, and the Central Statistics Office (CSO) identified kerosene as the main fuel/energy source for heating for 26% of people.

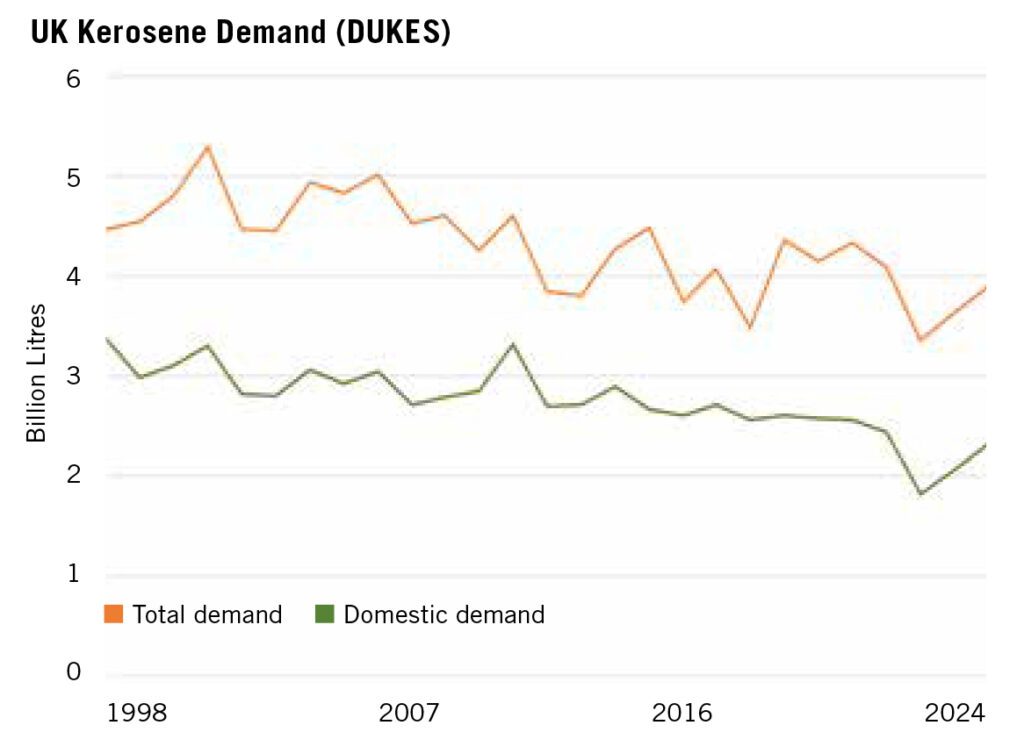

The first chart below shows total and domestic UK kerosene demand between 1998 and 2024 (Digest of UK Energy Statistics, DUKES), demonstrating a gradual 31% decline of domestic demand across 27 years, from 3.4 billion litres to 2.3 billion litres. This sustained fall highlights a long-term downward trend that is accelerating as new technologies and policies take hold.

Factors affecting demand

i. Price

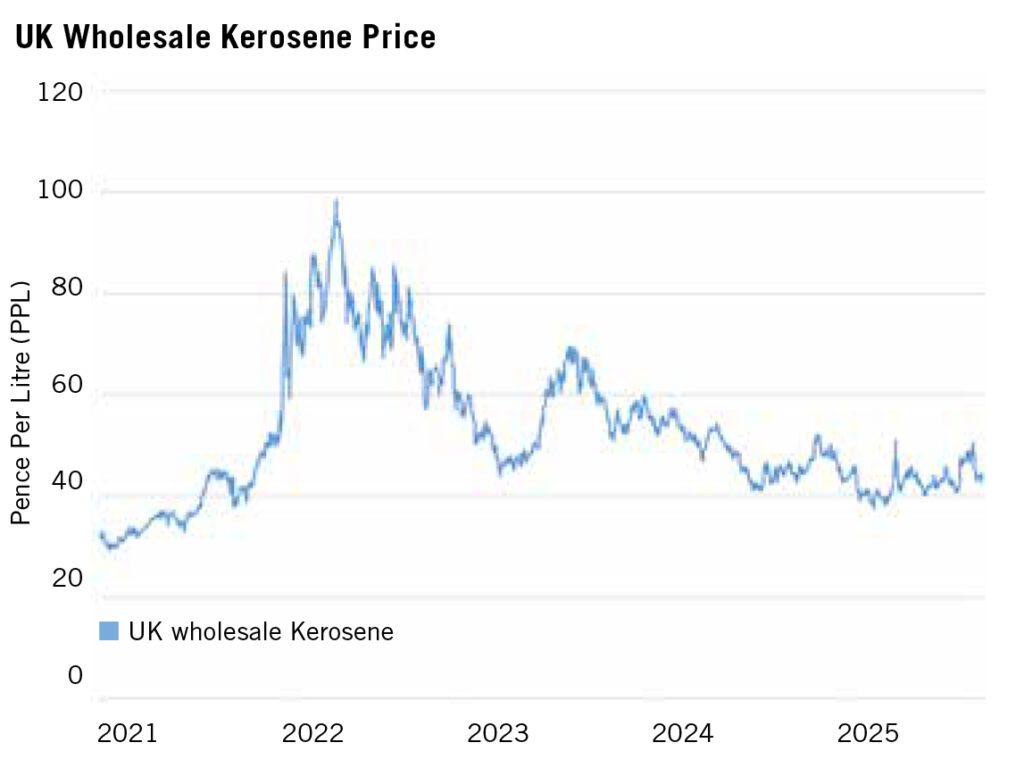

As a crude-oil derivative, the price of kerosene closely tracks global oil markets. Domestic demand is highly price-sensitive – domestic heating oil consumers typically purchase in bulk when prices are low. For example, low prices in 2020 (COVID-19) led to bulk buying despite steady demand. In 2022, demand dropped as prices spiked (Russia’s invasion of Ukraine), then recovered as prices eased in later years. The second chart demonstrates the volatility of UK wholesale kerosene pricing:

ii. Geography

Demand also varies by region; kerosene is far more common in rural/remote households that are not connected to the mains gas network. Whilst kerosene heats about 5% of UK homes, this figure rises to 20% in rural areas, such as the highlands of Scotland, South West England and East Anglia. Notably, 7 out of 10 areas where oil-only heating was most common were in the East of England (Office for National Statistics).

In Ireland, kerosene usage totals 18% in urban areas versus 41% in rural areas, and is the main source of heating for 43% of people in the Northern and Western Region (31% in the Southern Region and 14% in the Eastern and Midland Region). As demand is heavily localised, uneven demand patterns must be navigated by FODs, requiring targeted logistics, region-specific inventory planning, and rural delivery networks.

iii Seasonality

Another key demand factor is seasonality. Typically, demand rises in winter and falls as temperatures increase. Global oil demand typically peaks in the Northern Hemisphere winter as heating oil use rises from October, pushing prices up. However, analysts note a global shift in seasonality: warmer winters are cutting demand for heating fuels, while hotter summers are encouraging travel, increasing oil demand and prices in the third quarter.

The Met Office compared two 30-year periods (1961-1990 and 1991-2020), revealing average UK temperatures have increased by 0.8°C. The average coldest day of the year has become 1.7°C milder, and there are fewer ‘very cold’ days (where maximum temperatures do not rise above 0°C). Additionally, UKIFDA reported that the number of ‘heating degree days’ in the first nine months of 2024 was 2% below 2023, and 8% below 2019. Similar trends are observed in Ireland, where the average temperature has increased by 0.8°C compared to 1990 (Environmental Protection Agency).

However, demand for heating oil tends to follow price fluctuations more closely than temperature change (DUKES). For example, domestic oil consumption in the UK (88% of which is composed of kerosene), increased by 13% from 2023 to 2024, despite comparable temperatures. However, temperatures are projected to keep rising, with more frequent heatwaves expected, ultimately decreasing heating demand in the long-term.

Looking ahead, rising temperatures and more unpredictable weather patterns will increase operational volatility, requiring distributors to plan for both milder winters and sudden cold snaps

Consumer behaviour

As domestic kerosene demand is highly price-sensitive, increased prices may lead to smaller quantities being ordered, as consumers typically place bulk orders when prices are low. Additionally, higher prices increase the likelihood of theft, particularly in winter months when nights close in early and tanks are typically at their fullest. While theft can’t be fully prevented, OFTEC (The oil-heating trade body for the UK) advises homeowners to limit oil storage, meaning consumers may order smaller quantities more frequently.

Economic pressures may also affect consumer behaviour, with UK and Ireland households reducing energy use amid the cost-of-living crisis. The UK government suggests around 11% of households in England are classed as fuel poor, 34% in Scotland, 14% in Wales, and 24% in Northern Ireland. Notably, the total fuel poverty gap in England (energy cost reduction needed to lift all fuel-poor households out of fuel poverty), increased by an estimated 47% between 2020 and 2023.

With increasing consumer awareness of energy use and costs, pricing information is becoming more widely available. Online fuel marketplaces give consumers access to a wide range of suppliers, offering instant quotes and price comparisons.

SMEs, in particular, face heightened competitive pressure from large national suppliers with strong digital capability. As the online heating oil market grows, FODs must boost their digital presence and marketing and consider ways to deliver customer loyalty or risk falling behind competitors.

Finally, tank telemetry is an increasingly mainstream tool for domestic heating oil consumers, enabling tank level monitoring, usage tracking, and automated orders, reducing the risk of runouts and requirement for emergency deliveries. This directly impacts ordering behaviour, shifting it from manual bulk-orders to automated, more frequent top-ups.

While the minimum order quantity for domestic heating oil has traditionally been 500 litres, many FODs are now offering lower volumes, as an increasing number of customers search for 250, 300 and 400 litre prices (BoilerJuice). This trend increases delivery frequency relative to litres sold, putting pressure on operating costs unless route density and planning improve.

Ultimately, FODs may need to consider lowering their minimum order quantity to match current trends, whilst considering the impact of higher delivery and logistics costs, which may be passed on to the end-user.

Net zero and policy

To deliver net zero 2050, UK and Ireland governments are implementing several new policies that directly impact kerosene demand and drive significant sector change. The UK’s proposed phasing out of the installation of fossil fuel heating in existing homes off the gas grid has been delayed and eventually abandoned, but other initiatives, introduced by the Department for Energy Security and Net Zero (DESNZ), remain influential.

The ‘Future Homes Standard’ (FHS) which bans fossil-fuel boilers in new-build homes, is pending final legislation with implementation expected in 2026/2027, ultimately impacting kerosene demand.

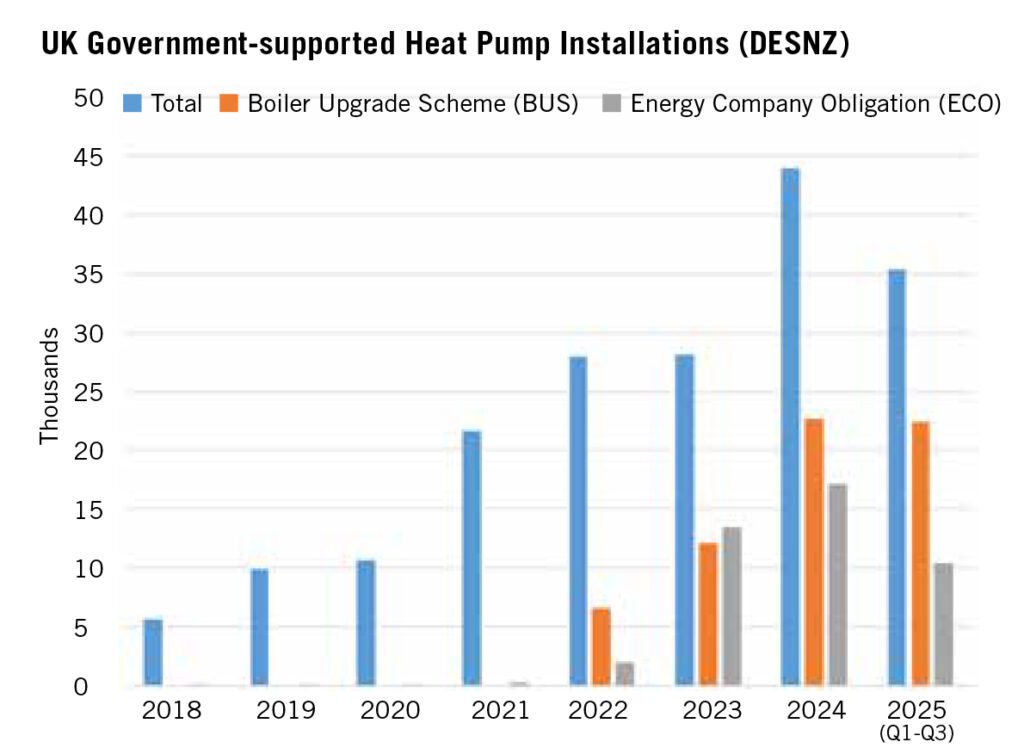

The UK government’s Clean Heat Market Mechanism (CHMM) encourages the deployment of low‑carbon heat pumps by obligating manufacturers to meet targets for installation in proportion to their fossil fuel boiler sales. The scheme operates from April 2025 until at least 2029. A 2023 government review suggested 600,000 installations are required by 2028 to make heat pumps a mainstream consumer solution, projecting that heat pumps will meet 65% of domestic heat demand, shifting the market towards low-carbon heating.

Financial incentives in the form of grants schemes such as the Energy Company Obligation (ECO) and the Boiler Upgrade Scheme (£7,500 grants) continue to encourage low-carbon heating adoption.

Heat pump installation numbers are rising steadily as the above chart indicates.

In Ireland, the CSO suggest 95% of new dwellings in 2023 used electricity-based heating (majority heat pumps), in the first three quarters of 2023, driven by NZEB regulations and SEAI support schemes. This compared with less than 5% in 2023 for fossil-fuel boilers (down from 79% for the period from 2010 to 2014).

Meanwhile, renewable liquid fuel alternatives, such as Hydrotreated Vegetable Oil (HVO), are gaining traction. The ‘Future Ready Fuel’ campaign – driven by industry trade bodies UKIKDA and OFTEC – cited a successful national demonstration in which 135 UK properties had boilers converted to HVO, reducing carbon emissions by up to 88% with no reports of diminished performance. Conversion costs are around £500 and can be completed in a couple of hours.

However, the wider rollout of HVO, jointly called for by the industry trade associations, depends on government implementation of the UK’s Renewable Liquid Heating Fuel Obligation (RLHFO). In Ireland, the government is pressing ahead with a Renewable Heat Obligation including blended heating fuels such as a kerosene / HVO mix.

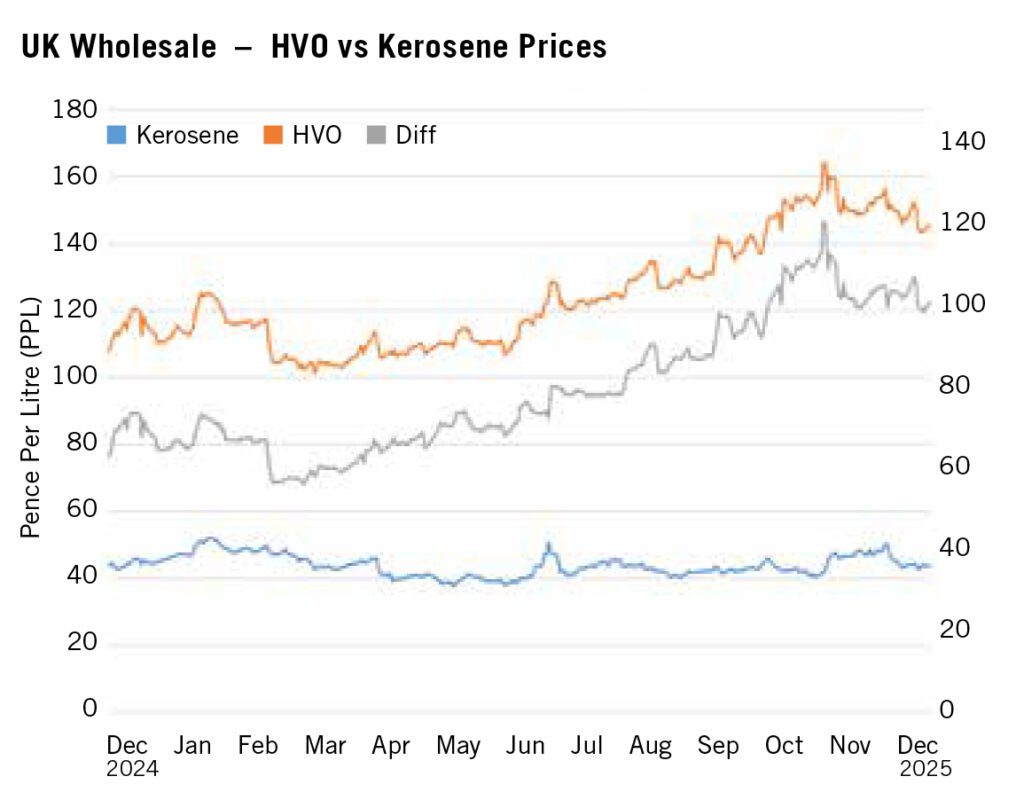

The wholesale price differential between kerosene and HVO remains significant and is also significant in its impact on uptake. This price differential remains the key barrier to rapid uptake, limiting consumer adoption without policy intervention. The chart (above right) demonstrates the difference between UK wholesale Kerosene and wholesale HVO over the last 12 months.

Summary

The domestic heating sector in the UK and Ireland is undergoing rapid and multi-layered transformation. Climate variability, namely rising temperatures and more frequent extreme weather events, is disrupting long-established seasonal demand patterns, while economic pressures are making consumers more cost-conscious, further intensifying price sensitivity of domestic kerosene demand and reshaping long-established demand patterns.

Meanwhile, digitalisation, telemetry and online marketplaces are redefining how consumers purchase heating oil.

Broader net zero commitments are steadily shifting demand toward low-carbon heating systems, reducing long-term kerosene consumption. Although this transition will take time, due to the numerous barriers around cost, workforce and time, policy signals are clear.

For FODs, the challenge is to be aware of developments and adapt operating models before these shifts materially affect margins, delivery efficiency and customer retention.

Strong regional demand in rural areas reinforce the importance of efficient route planning and control of delivery costs. Online marketplaces make competitive pricing, increased digital presence and online engagement essential in order to remain competitive.

Additionally, economic pressures, theft concerns and growing use of telemetry have increased demand for smaller, more frequent top-ups. This may suggest a need for revised minimum order quantities and pricing strategies, coupled with improved planning systems.

Looking ahead FODs should:

Prepare for increasing climate volatility, whether milder winters or cold snaps, to manage stock and operational readiness.

Stay closely aligned with evolving policy frameworks and government initiatives that are accelerating the shift from fossil-fuel heating to low-carbon alternatives.

Be ready for a mixed-fuel future that includes heat pumps, HVO and blended solutions.

By diversifying offerings, investing in digital tools and aligning with customer expectations, distributors can continue to play a central role in home heating – even as the energy landscape changes.

FOD Action Plan: How to stay competitive as buying patterns change

1. Demand and stock management

- Increase frequency of demand review, as buying patterns become more volatile.

- Review stockholding strategy for winter vs shoulder seasons.

- Build contingency plans for extreme-weather spikes (rapid stock procurement, emergency routing, overtime budgeting).

- Model the impact of various demand decline scenarios to support investment planning.

2. Pricing and margin strategy

- Review the impact of online marketplaces on pricing strategies

- Deliver clear price-communication – transparency builds loyalty.

- Offer incentives for larger drop sizes (e.g., loyalty credits, discount bands).

- Track competitor pricing daily during peak season.

3. Delivery economics and operations

- Reassess minimum order quantities – consider flexing to meet market expectations.

- Strengthen route optimisation capability to counter smaller, more frequent orders.

- Analyse drop size vs cost-to-serve by postcode sector.

- Expand rural cluster delivery options (longer lead times, grouped runs).

- Reduce emergency deliveries by encouraging telemetry adoption.

4. Customer behaviour

- Improve online quoting options

- Implement a digital loyalty or subscription-based top-up plan.

- Promote telemetry with clear customer ROI messaging (avoid runouts, smoother budgeting).

- Integrate theft-prevention advice with seasonal customer communications.

5. Energy transition readiness

- Track local heat pump deployment – identify areas where kerosene decline will appear first.

- Evaluate the opportunity to offer HVO (blend or 100%) and associated tank services.

- Ensure customer-facing teams are able to communicate low-carbon options.

- Stay up to date with policy developments since it will shape demand.

- Talk to customers about their current and future preferences.

6. Business diversification

- Explore revenue streams beyond kerosene (HVO, lubricants, service plans, energy efficiency upgrades, alternative technologies).

- Invest in digital tools that improve forecasting, routing and customer service.

- Build partnerships (installers, trades, energy-efficiency services) to stay relevant as heating systems evolve.

- Continually review fleet strategy – consider vehicle size mix and fuel type for future conditions.